Wool is back in vogue!

15 September 2023

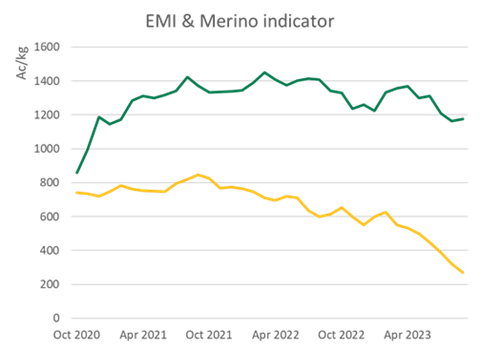

Key points: The (Eastern Market Indicator) EMI has outperformed all lamb and sheep indicators this year The difference between the EMI and Merino lamb price is growing Expect to see sheep producers…